Update: Weekly Strategies

Comments and performance

Update on April 3, 2026: In case you are forwarded here from a Price Action Lab Blog email campaign, please click here for the correct article.

The S&P 500 index fell 2.1% this week. The stock market has been going down for five weeks in a row, and the drop from the all-time highs of January 27 has grown to 8.6%.

The cross-sectional momentum for sectors and assets increased by 0.6% and 0.1%, respectively, this week. The Dow-30 long-short, which dropped 1.4%, was the source of the disappointment. Because of their positions in materials, utilities, and commodities, the cross-sectional momentum strategies filled the gap left by the long-short strategy’s inability to provide some convexity due to a whipsaw in the large-cap market.

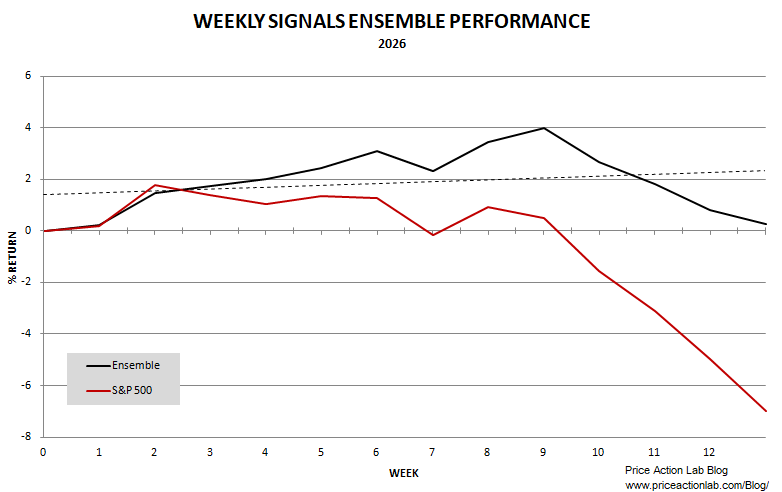

The six-strategy ensemble’s average year-to-date return is 0.2%, while the benchmark (the S&P 500 index) has lost 7%. As a result, this week’s performance spread went from 580 to 720 basis points.

Asset cross-sectional momentum has been the best-performing strategy so far this year, with a 7.3% gain. This strategy held a long position in gold (IAU) from March 2024 to the end of 2025, which saw a gain of 108%. Due to a long position in a commodity ETF, this strategy has so far offered a diversification benefit.

During another week of market turmoil, the ensemble reached its main goal. We can’t predict how asset prices will move in the future, unlike a lot of market analysts on social media and blogs. In the face of increasing uncertainty, we hope that our strategies will continue to provide convexity and that the ensemble will perform significantly better than the benchmark in the future.

Note that the strategies in the weekly ensemble cover tactical asset allocation, mean reversion, cross-sectional momentum, and equity long-short. Click below for more information.