The New Quantitative Easing

The New Quantitative Easing

From Printing Money to Selling Crude Oil

In 2008, the US economy needed quantitative easing to avoid a deflationary cycle due to a financial crisis. The crisis was averted, but the economy became addicted to free money. The pandemic extended quantitative easing into 2020, with the Fed balance sheet rising to $9 trillion in April 2022. The supply shock due to the pandemic and the free money were the main drivers of the inflation cycle that started in February 2021 and peaked in June 2022, with the YoY CPI rising to 9.06%.

The US economy needed medicine, but not in the form of excessive rate hikes because that would cause a deep recession just before an election year. The new quantitative easing came in the form of sales of strategic petroleum reserves (SPR).

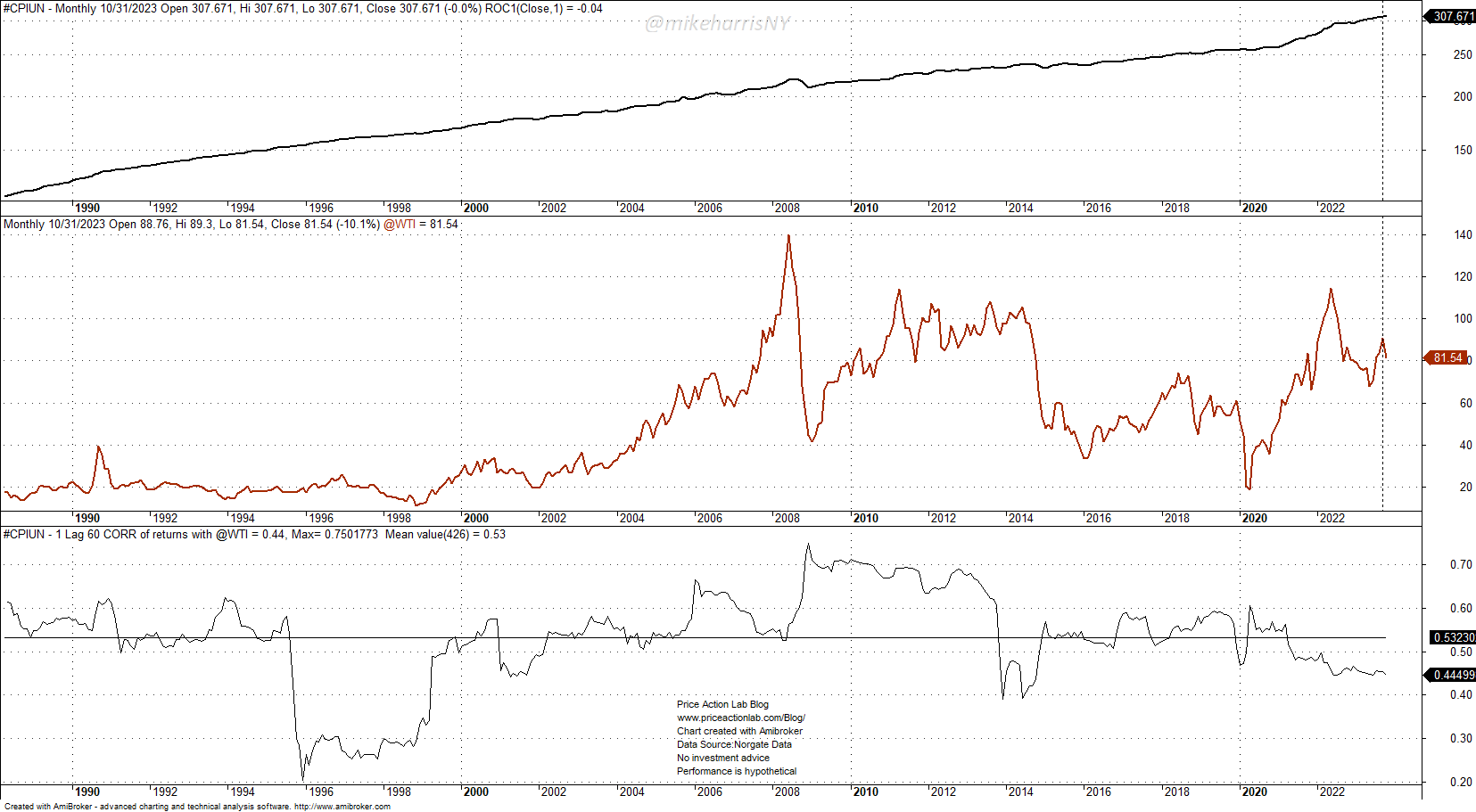

The correlation between the CPI and crude oil was well-known: changes in crude oil explained a good fraction of the change in the CPI with a small delay.

The average 60-month correlation of the CPI and crude oil percent changes lagged by a month has been 0.53. The minimum has been about 0.2, and the maximum is 0.75. Since 1988, the correlation has been positive and close to the long average for the most part.

Given the high correlation between the CPI and crude oil, the new quantitative easing for the economy took the form of “commodity easing,” specifically flooding the market with cheap oil from the SPR.

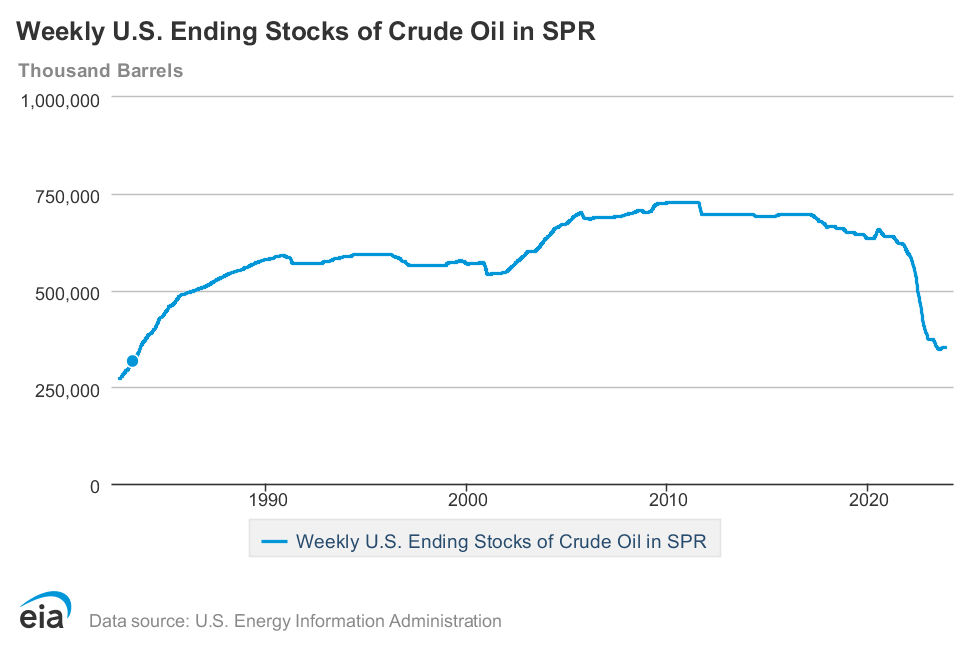

Between July 2020 and November 2023, the reserves plunged about 46% back to around 1986 levels!

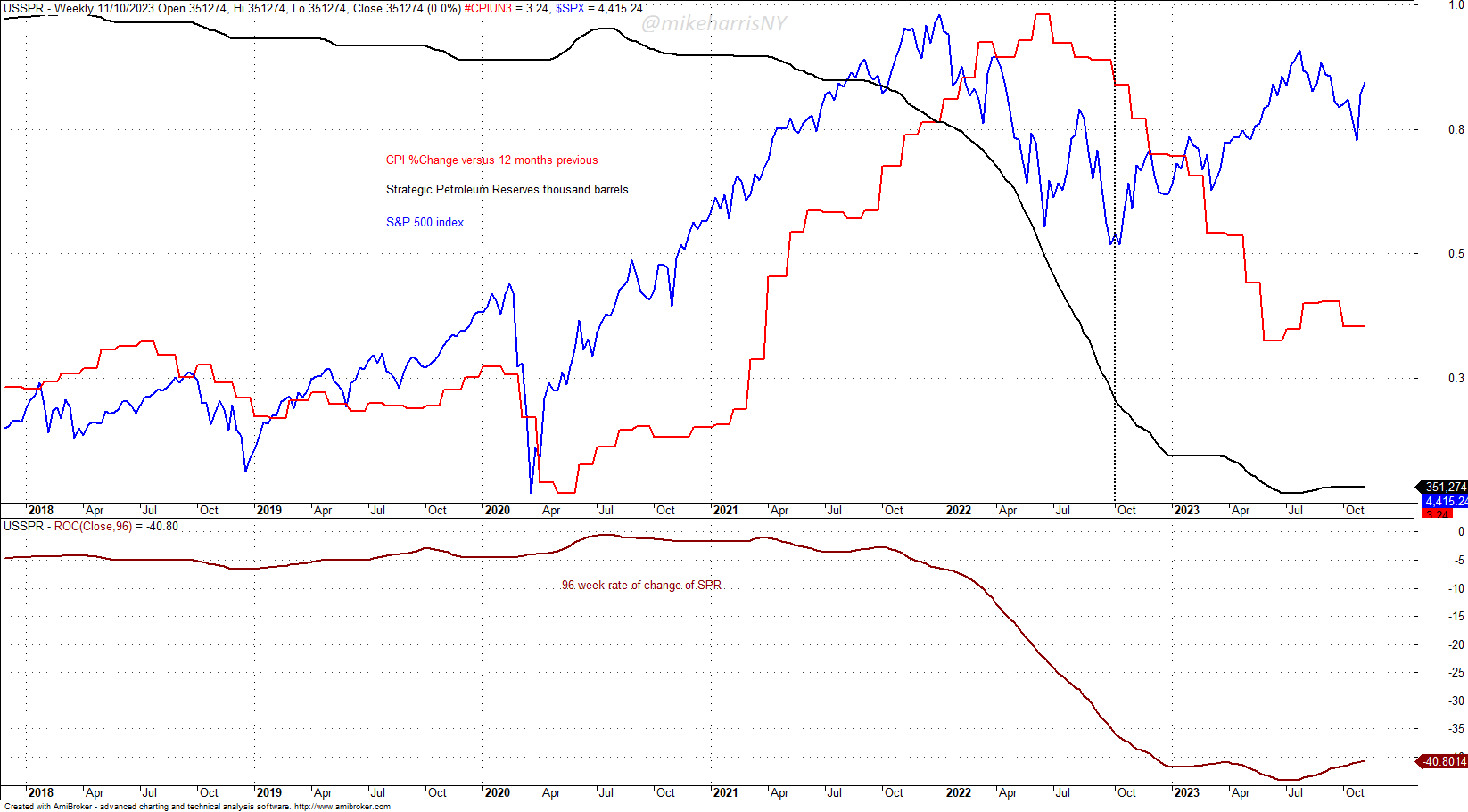

The “commodity easing” program, in conjunction with a moderate rise in interest rates, was a success. In the course of 12 months, from June 2022 to June 2023, the YoY CPI fell from 9.06% to 3%.

Due to falling inflation, the stock market started discounting future rate cuts. The correction ended in September 2022, and a rebound started while the sales from SPR continued in full force. The vertical dotted line in the above chart shows when investors realized there was a new regime of interventions, what is called in this article “commodity easing”.

What could go wrong?

Unexpected events related to geopolitics could cause a spike in crude oil and inflation to rise again. The US stock market is sensitive to high inflation due to its core, the tech sector, having a long duration. Therefore, politicians have started realizing that it is to the benefit of the economy to normalize relations with China and possibly in the future with Russia, but the latter could take a long time. Hence the recent meeting with the Chinese President. The US depends on cheap Chinese exports to keep inflation under control. China exports deflation to the US and the US exports inflation to China. Therefore, normalizing relations with China is a prudent path to take. The situation with Russia is much more complex, and there are risks only in the case of a direct conflict since their exports do not have a direct impact on the US CPI. In this case, game theory equilibrium may be the desired course for the time being.

In the Price Action Lab Blog, we offer premium content that includes the weekly Price Action Lab Report and weekly systematic trading signals for ETFs and equities.

By subscribing, you have immediate access to hundreds of articles. Premium Articles and Market Signals subscribers have immediate access to all articles in the trader education section, and All in One subscribers have immediate access to all premium content, including more than 140 Premium Insights articles.

We also offer daily mean-reversion signals for SPY, QQQ, and ZN futures.

Disclaimer: No part of the analysis in this blog constitutes a trade recommendation. The past performance of any trading system or methodology is not necessarily indicative of future results. Read the full disclaimer here.

Charting and backtesting program: Amibroker Data provider: Norgate Data

If you found this article interesting, you may follow me on Substack and X.

Do you have performance information for your various signal services?