Systematic Trading—Year-To-Date Update

Performance of monthly, weekly, and daily strategies

Performance is without any leverage. There is no use of futures contracts and trading on margin, as this complicates the estimation of risk parameters, including the Sharpe ratio and the risk-adjusted alpha. All performance metrics are calculated based on the applicable trading timeframe.

Monthly Signals

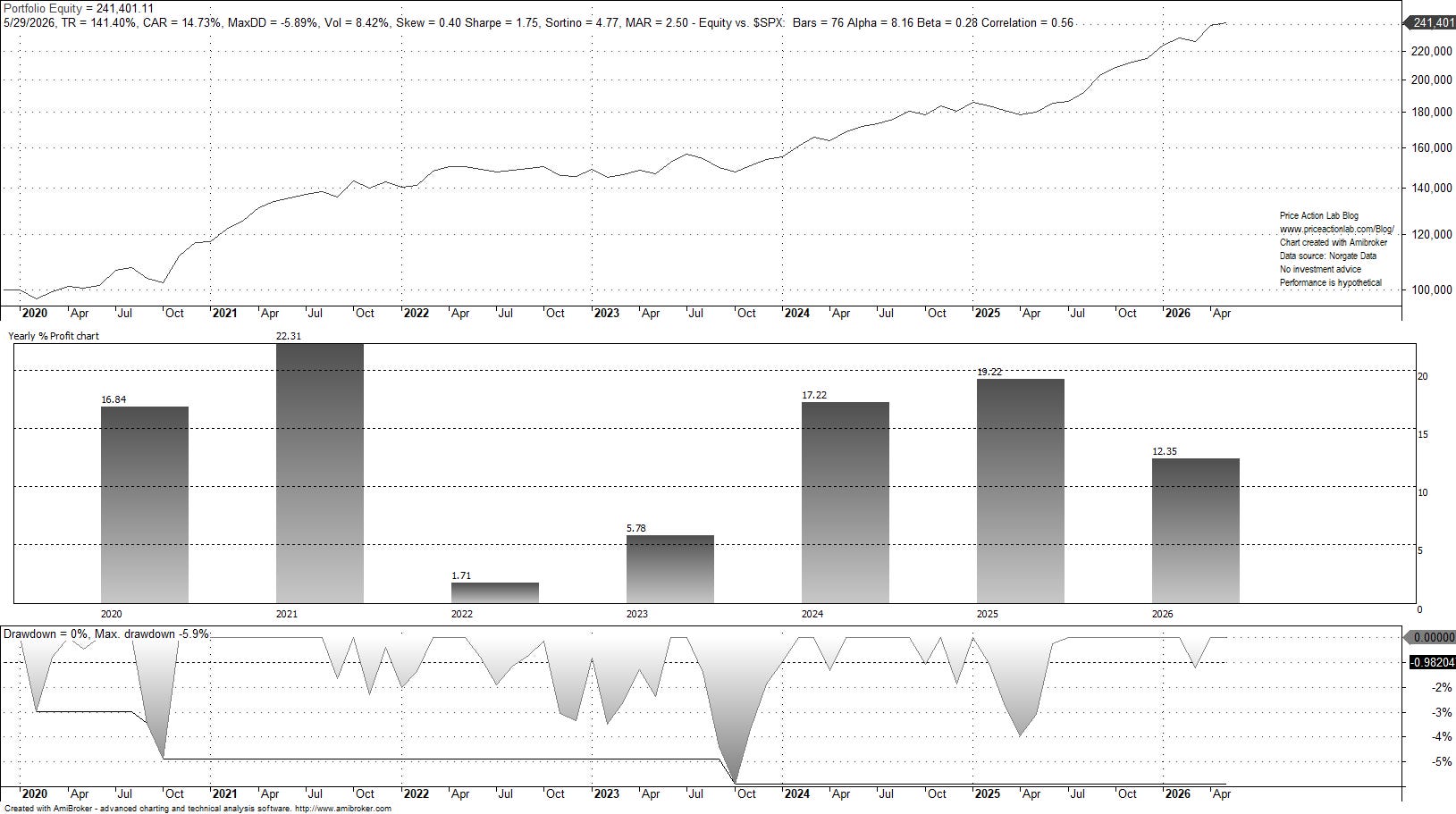

Hybrid Asset Allocation

The hybrid asset allocation ensemble of two strategies (HAA) gained 1.2% in May 2026, after surging 5.5% in April 2026, and it is up 12.3% year-to-date.

Since 2020, the Sharpe ratio of HAA is 1.74 versus 0.94 for the buy-and-hold SPY ETF. The risk-adjusted alpha is 8.1%, and beta is 0.28. Maximum drawdown is only 5.9%. Click here for more details and the last update on May 29, 2026.

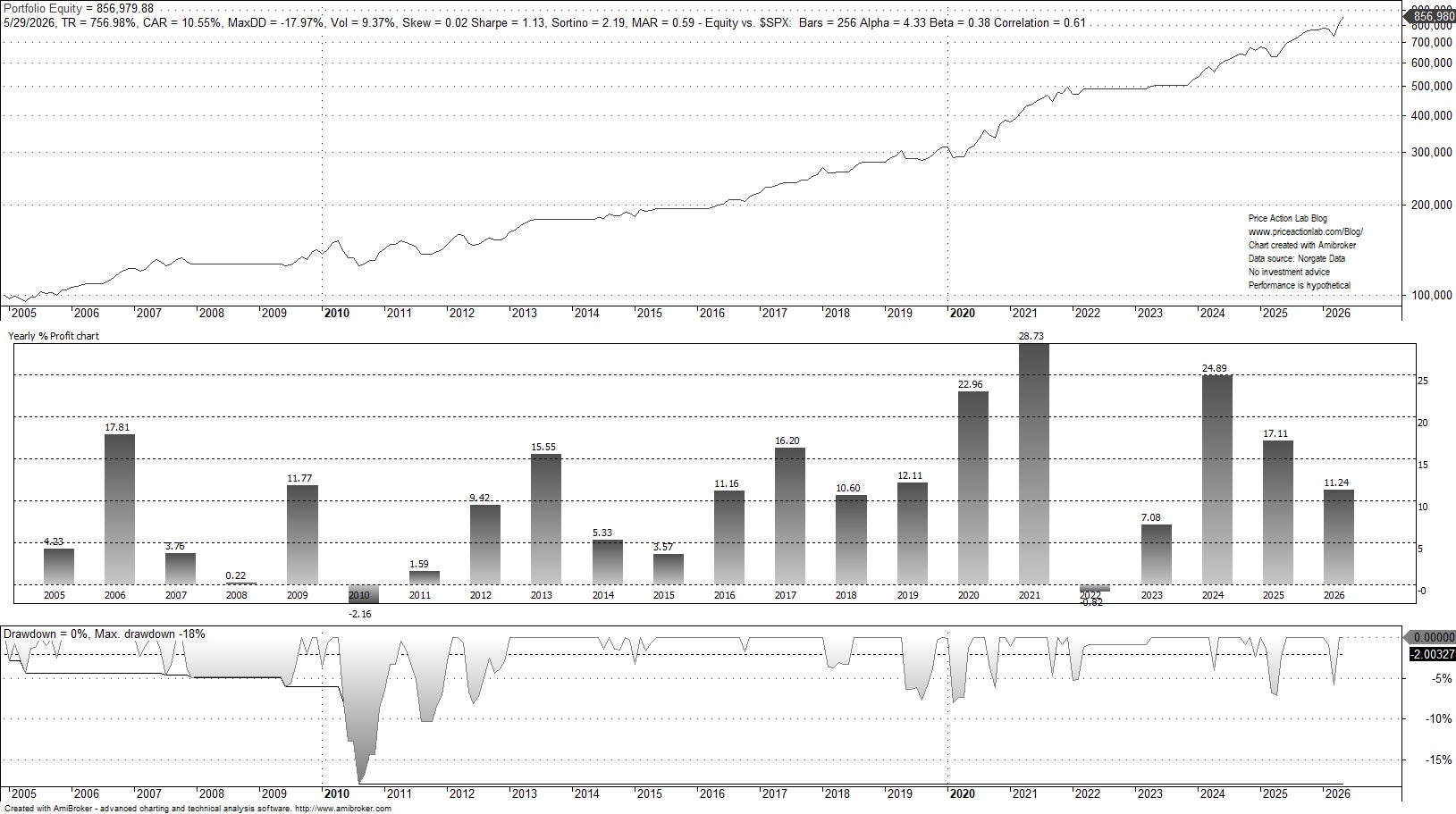

Dynamic momentum

Dynamic momentum (DYNMOM) gained 5.3% in May 2026, after surging 10.5% in April 2026, and it is up 11.2% year-to-date, due to tracking the SPY ETF since May of last year.

Since the inception of the SPY ETF, the Sharpe ratio is 1.13. The risk-adjusted alpha is 4.3%, and beta is only 0.38. The maximum drawdown is 18%. Click here for the last monthly update on May 29, 2026.

Weekly Signals

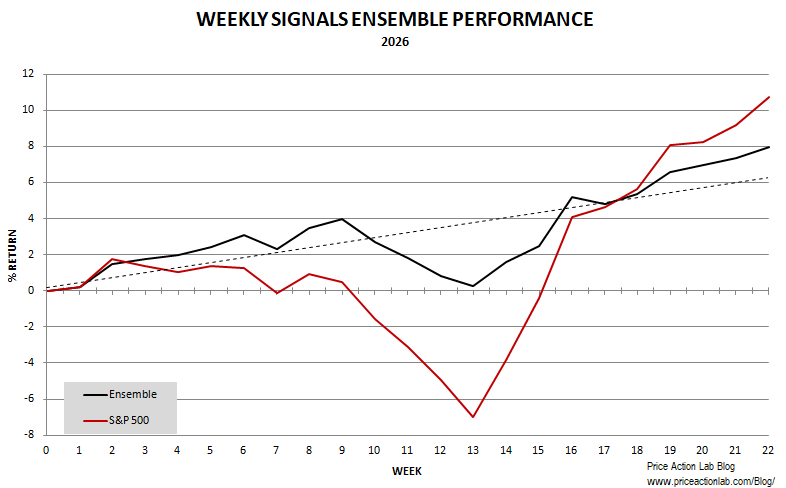

1. The ensemble of the six strategies gained 2.5% in May 2026, +7.9% YTD.

The ensemble of the six strategies has achieved its primary objective, which is high risk-adjusted returns. Year-to-date, the ensemble outperforms with MAR (return/drawdown) at 2.19 versus 1.24 for the S&P 500 index benchmark. The ensemble targets an annualized return of about 8% at less than 8% volatility, or a Sharpe ratio higher than 1. Click here for the last update and more details.

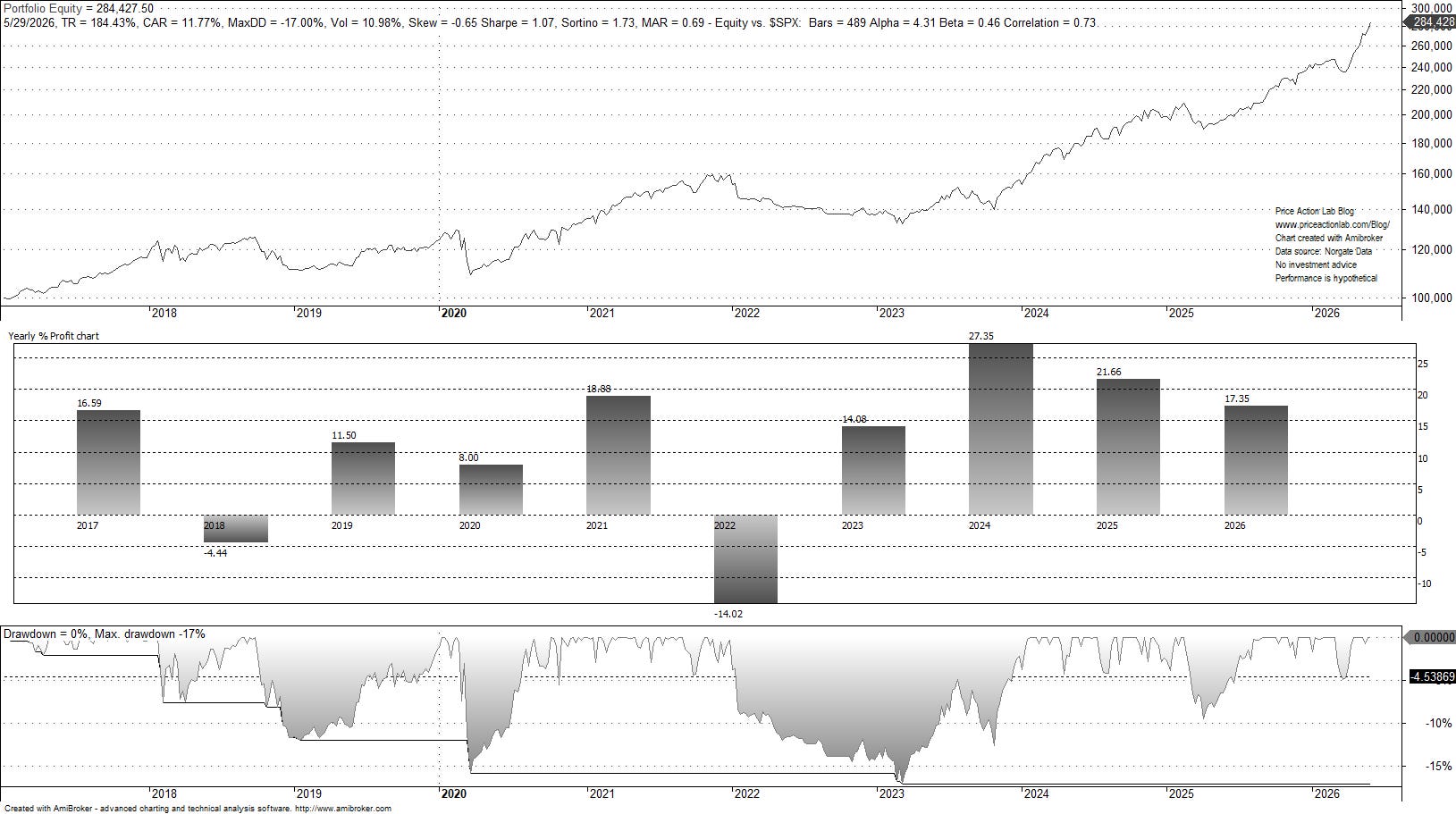

2. The ensemble of the two strategies in our weekly reports gained 2.8% in May 2026 and is up +17.2% for the year (+19.8% when returns are calculated after annual rebalancing).

The Sharpe ratio is 1.13. The risk-adjusted alpha is 4.3%, and beta is 0.46. The maximum drawdown is 18%. Click here for the last report on May 29, 2026.

Daily Signals

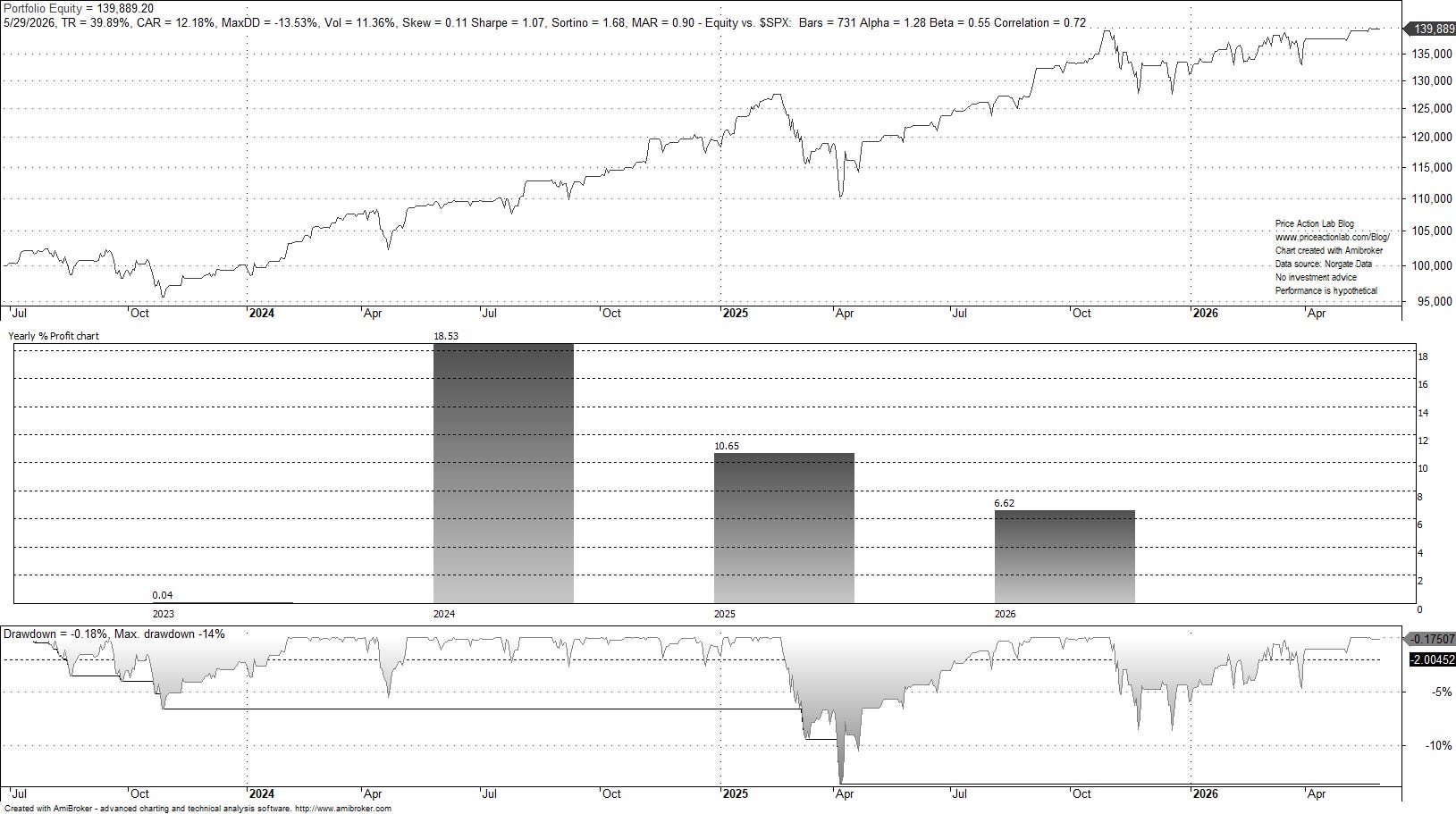

Daily mean reversion gained 1.3% in May 2026 and is up +6.6% YTD. Below is the equity performance since the start of the daily mean reversion signals subscription on June 27, 2023. Note that occasionally, daily mean reversion makes use of 2x leveraged ETFs.

The Sharpe ratio is 1.07, and the maximum drawdown is 13.5%. Click here for the latest update and for the performance of two bonus strategies.

Transparency Statement and Disclaimer

Our daily, weekly, and monthly signals are transparent about signals and positions, and there is no ambiguity. We report all entries and exits in advance for the open of the following day, week, or month. We do not make vague claims about entries and exits depending on whether the price action was favorable or not. No ambiguity, no buzzwords, no macro analysis: well-defined entry and exit signals for major and liquid ETFs and equities from robust systemtic strategies.

The monthly, weekly, and daily signals are available on the Price Action Lab Blog. The weekly two-strategy ensemble signals are also available in our weekly report on Substack.

The signals are provided for informational purposes only and do not constitute investment advice or actionable content. We do not warrant the accuracy, completeness, fitness, or timeliness of the signals for any particular purpose. Under no circumstances should the strategies be treated as financial advice.

Strategy Package

The purpose of the package is to provide informational content that aids in the development of trading strategies towards becoming a professional trader or even establishing a hedge fund. The package provides the rules for a total of 16 trading strategies plus the PSI5 algorithm.